Valued at a market cap of $94.7 billion, Intercontinental Exchange, Inc. (ICE) is a global financial infrastructure provider that operates exchanges, clearinghouses, and data platforms, most notably owning the New York Stock Exchange. The company facilitates trading across asset classes, including equities, derivatives, fixed income, and commodities, while also generating revenue from listing and transaction fees. Over time, ICE has expanded beyond traditional exchange operations into data services and technology solutions, positioning itself as a diversified player in capital markets.

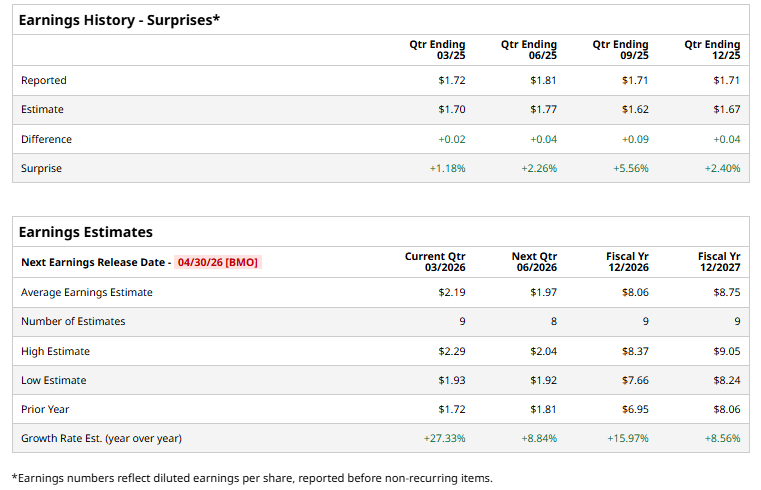

The financial giant is gearing up to announce its Q1 2026 earnings report before the market opens on Thursday, Apr. 30. Ahead of the event, analysts expect ICE to report an EPS of $2.19, up 27.3% from $1.72 reported in the year-ago quarter. Moreover, the company has a robust earnings surprise history. It has surpassed the Street’s bottom-line estimates in each of the past four quarters, which is impressive.

For fiscal 2025, ICE is expected to report an EPS of $8.06, up 16% from $6.95 reported in 2025. In fiscal 2027, its EPS is expected to further surge 8.6% year over year to $8.75.

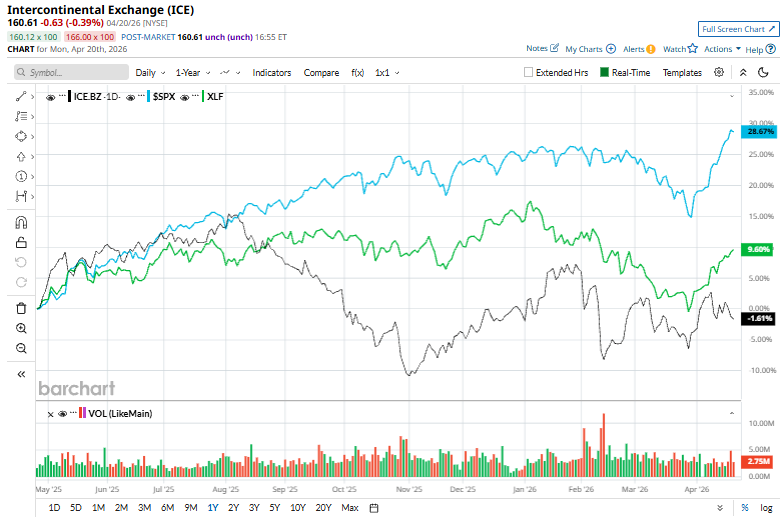

The stock has gained 1.2% over the past 52 weeks, trailing the S&P 500 Index’s ($SPX) 34.6% returns and the Financial Select Sector SPDR Fund’s (XLF) 12.8% gains during the same time frame.

On Mar. 10, shares of Intercontinental Exchange fell around 3% as broader weakness in the asset management sector weighed on sentiment. Investor concerns about rising risks in the private credit market, particularly potential loan defaults and redemption pressures in Business Development Companies (BDCs), dampened confidence across financial-related stocks.

However, analysts remain highly optimistic about ICE’s prospects, maintaining a consensus “Strong Buy” rating overall. Of the 17 analysts covering the stock, 13 recommend a “Strong Buy,” two suggest a “Moderate Buy,” and two advise a “Hold.” Its mean price target of $199.94 implies a 24.5% upside potential from current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Raymond James Is Betting Okta Stock Can Gain from Here. Should You Buy Shares Now?

- Massive and Unusual Trading in Home Depot Call Options - Is the HD Stock Rally Over?

- Will Q1 Earnings Power GE Vernova Stock to $1,225?

- PayPal Stock Is Down More Than 80% Over the Past 5 Years. Michael Burry Is Buying the Dip.