Qualcomm (QCOM) investors are about to get a reality check on April 29 when it reports its second quarter of fiscal 2026 earnings. It is not because the company is weak, but because it must prove that its strong momentum over the past few years can withstand a slowing smartphone cycle and increasingly cautious analyst forecasts.

A Strong Quarter, but Risks Are Rising

Valued at $144.6 billion, Qualcomm is a semiconductor and tech company that designs chips and software powering smartphones, cars, computers, and connected devices. Qualcomm entered fiscal 2026 with solid momentum, with revenue rising 5% year-over-year (YoY) to $12.2 billion and earnings increasing by 3% to $3.5 per share. Its semiconductor division, QCT, generated $10.6 billion in revenue, an increase of 5% YoY. Handset chip sales alone accounted for 73% of overall QCT revenue but only increased 3% YoY.

While declining handset sales are a concern, automotive sales stood out, reaching $1.1 billion, up 15% YoY. The company has secured significant partnerships, including a long-term supply agreement with Volkswagen Group (VWAGY) and collaborations with major automakers such as Audi and Porsche (POAHY). In IoT, revenues reached $1.7 billion, growing 9% YoY, owing to strong demand in industrial, networking, and consumer applications. Qualcomm is rapidly pushing into industrial computers, smart cameras, drones, and edge AI systems with its Dragonwing platform. The company also reported $1.6 billion in revenue for the QLT segment, its licensing business, fueled by strong global handset demand, particularly in premium and high-tier devices.

Furthermore, Qualcomm’s strategic acquisitions are strengthening its long-term positioning in the semiconductor space. It completed the acquisition of Alphawave Semi to enhance high-speed connectivity capabilities and acquired Ventana Micro Systems to expand its RISC-V CPU development for data centers.

The Core Problem Now

Qualcomm is still heavily dependent on smartphones, and that segment is entering a weak phase. Rising AI data center demand is causing a global memory crunch, putting pressure on smartphone production. OEMs are reducing inventory and scaling back production, particularly in China. The company is actively trying to reduce its dependence on smartphones and expand its automotive and IoT segments, but diversification is going slower than expected, hampering earnings.

JPMorgan agrees that the company’s diversification is going slow and there are no near-term catalysts to support its growth. The firm believes Qualcomm’s QCT Handsets revenue could decline by 22% in 2026. The firm downgraded QCOM stock to “Neutral” from “Overweight” while reducing its price target to $140 from $185. This is probably why, despite strong Q1 results, Qualcomm has issued weak guidance and analysts have a cautious outlook for fiscal 2026.

Why Do Q2 Earnings Matter So Much for QCOM Investors?

For the second quarter, Qualcomm expects revenues between $10.2 billion and $11 billion, compared to $11.6 billion in Q1 2025. Adjusted EPS could fall to a range of $2.45 to $2.65, compared to $3.41 in the year-ago quarter. Management expects handset sales to decline to around $6 billion due to memory constraints, while IoT is expected to grow at a low-teens rate. Meanwhile, automotive revenues could accelerate by more than 35% YoY. This outlook reflects a transition phase where traditional smartphone growth faces headwinds, but newer segments are beginning to take the lead.

In fiscal 2026, analysts predict a 1.2% drop in revenue to $43.6 billion, followed by a 7.8% drop in earnings to $11 per share. Revenue and earnings are expected to remain largely flat into 2027.

In the Q2 report, investors should watch out for clarity on memory constraints, signs of stabilization in handset demand, and continued momentum in automotive, IoT, and AI-driven businesses, as well as management’s guidance for the full year. This will allow them to assess whether Qualcomm can navigate short-term supply disruptions while maintaining its long-term growth trajectory and whether the stock is worth holding on to.

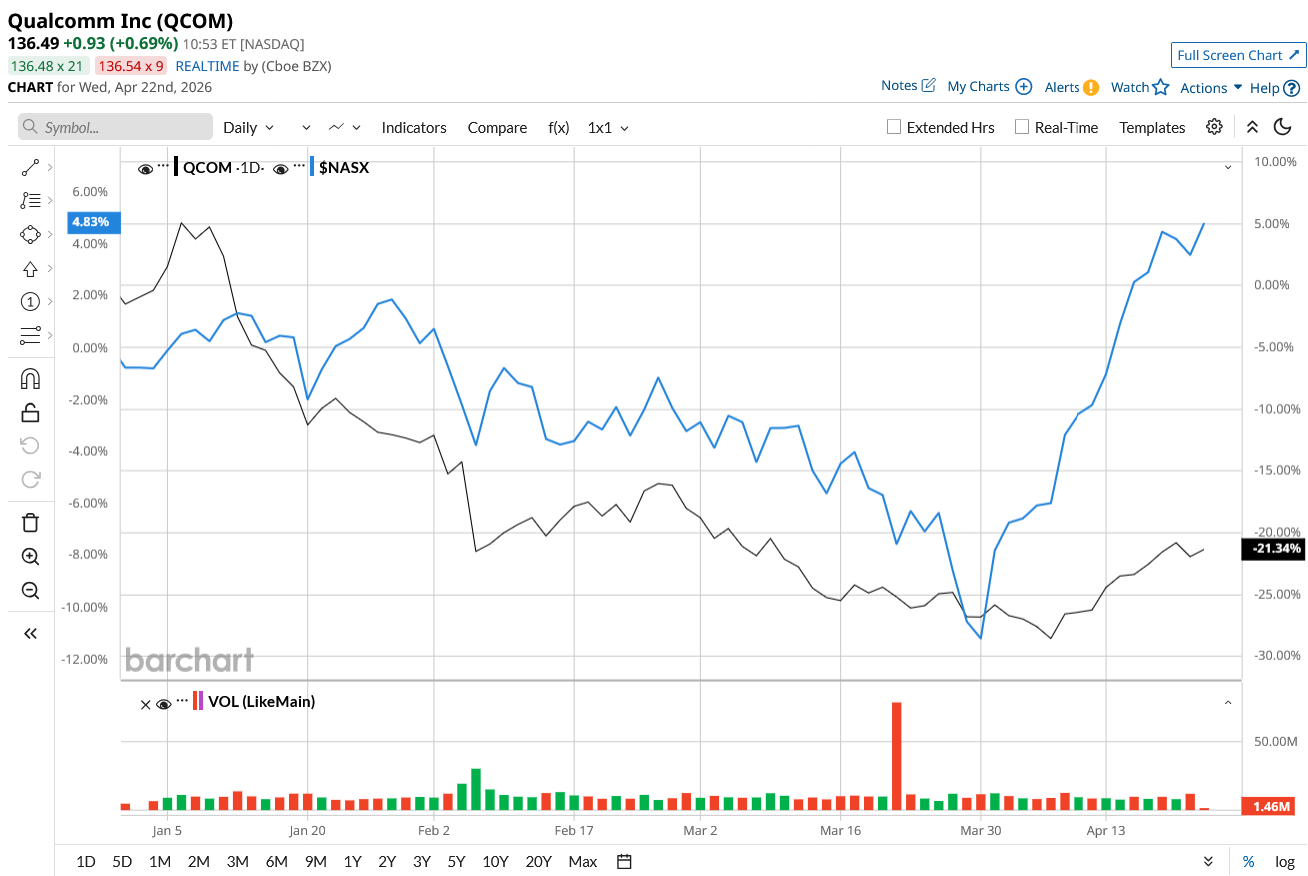

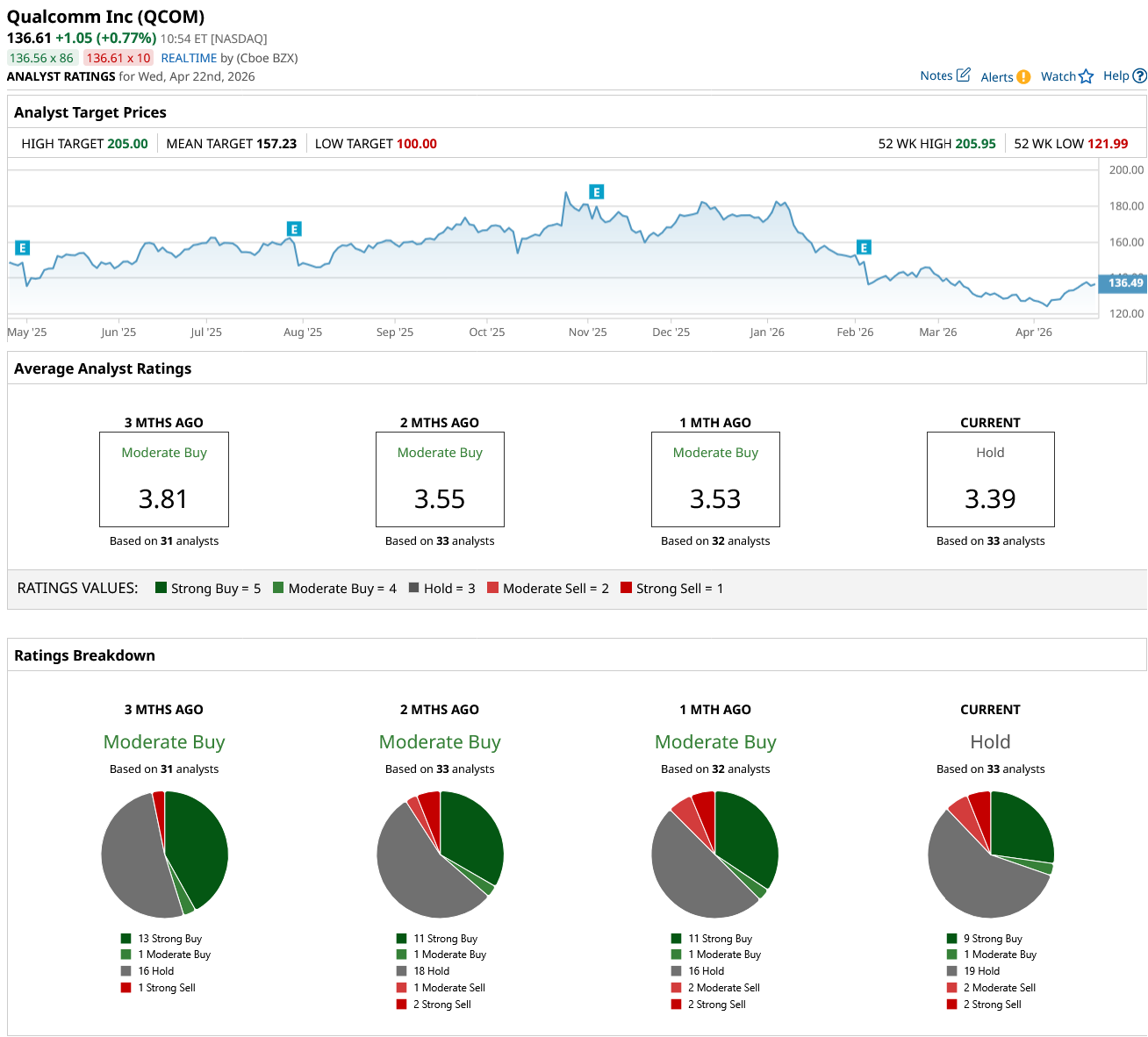

While Wall Street rates the stock as an overall “Hold,” analysts believe the stock has more room to run in the coming months. QCOM stock is down 20% year-to-date (YTD), compared to the broader market gain of 4.4%, and has fallen 33% from its 52-week high of $205.95. Based on its mean target price of $157.23, the stock could surge 15% from current levels. Plus, its high target price of $360 implies an upside potential of 51% over the next year.

Of the 33 analysts covering the stock, nine rate it a “Strong Buy,” one says it is a “Moderate Buy,” 19 recommend holding it, while two say it is a “Moderate Sell,” and two rate it a “Strong Sell.”

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Should You Buy the Dip in United Airlines Stock?

- Axe Compute Soars on $260M Nvidia Deal. Is It Too Late to Buy AGPU Stock?

- This Delta Insider Just Slashed His Stake by More Than One-Fifth (21%). Is It Time to Follow Suit and Ditch DAL Stock?

- AMD Stock Just Hit New All-Time Highs. Should You Buy Shares Here?